Budgeting for Homeschool Families: Does the thought of budgeting make you nervous? Does thinking about financial issues keep you up at night? Managing our money wisely (and realistically) as homeschool families is extremely important, but it can feel overwhelming to even know where to start. This video interview is for you!

I recently spoke with my friend Matt Miner, a CFP® and Advisor with PLC Wealth Management in Raleigh, NC …and a homeschool dad of 3 children. We talked all about budgeting for homeschool families, planning for our children’s futures (and our own), realistic grocery budget planning, helpful books/resources for future study, and more!

Check out the video and show notes below, discuss them with your spouse, and share them with your friends! (Plus: BONUS Mini-Episode at the end of the post!)

Who is Matt Miner?

Matt earned his MBA at Duke University’s Fuqua School of Business with concentrations in Marketing and General Management, and his undergrad degree from Arizona State University in Finance. Matt’s focus is helping others do a great job managing their money. His love of personal finance grew out of his family’s journey to repay nearly $250,000 in student loans within about three years of completing graduate school. Since then, Matt has worked to provide resources and coaching in this important area.

Matt lives in Raleigh with his wife Charity and their three amazing children, Lucy, Josh, and Ben. Matt loves spending time with his family, writing, running, hunting, and doing carpentry projects around the house. You can read more about Matt and his thoughts on money at Work Pants Finance, at LinkedIn, or contact him directly.

Budgeting for Homeschool Families:

{This post contains paid links. Please see disclaimer.}

Show Notes {with video time stamps}

What is a Budget? Why is budgeting important? Is it as complicated as we think? {3:55}

“A budget is telling your money where to go, instead of wondering where it went.” John Maxwell via Dave Ramsey

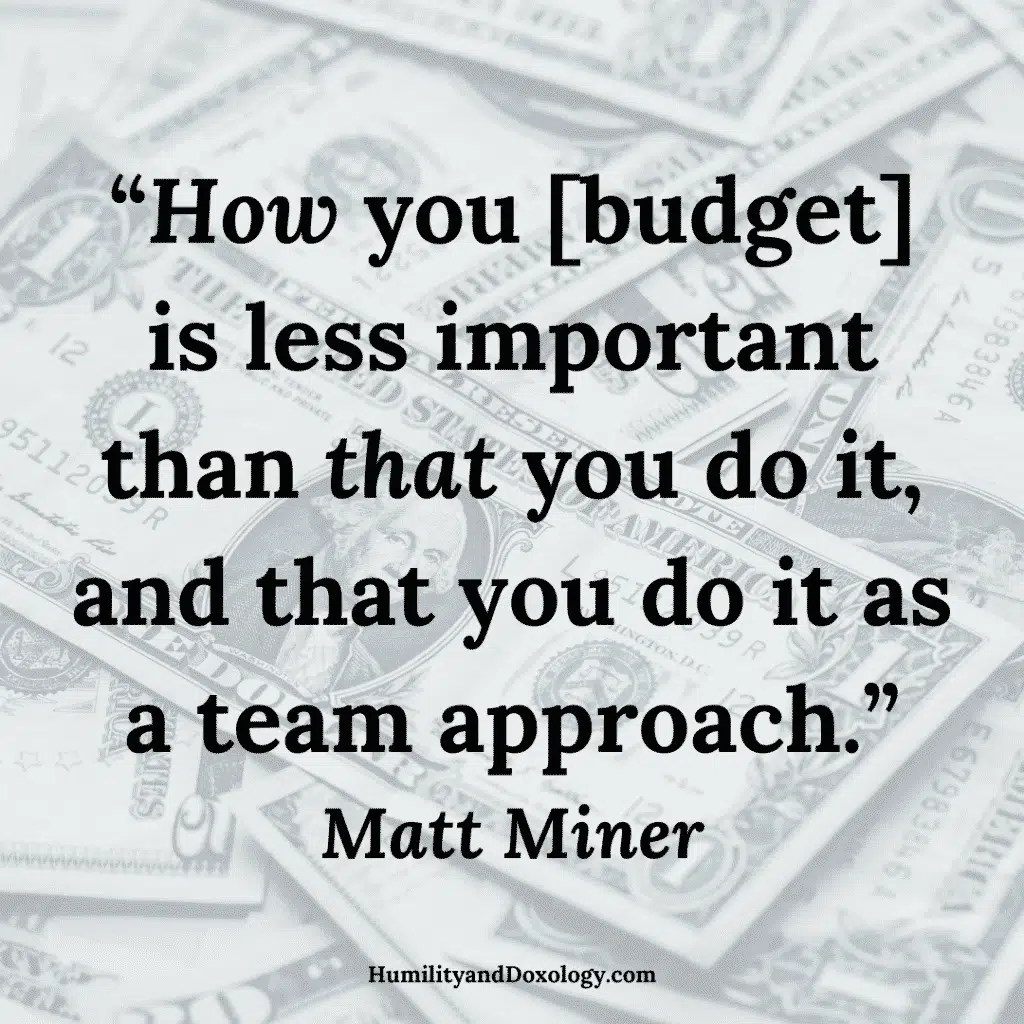

“How you [budget] is less important than that you do it and that you do it as a team approach.” Matt Miner

Detailed Budget -v- Anti Budget {4:50}

Matt recommends starting, especially if you’re dealing with debt, with a Detailed Budget. This means looking first at your Gross Income, then moving on to Giving, Saving/Investing, and other Spending areas. Yes, you’ll be tracking dollar for dollar at first.

It’s a really big project. But if we engage in that for 2-4 months, Matt assures us, we will really have an accurate picture of what we’re currently doing and can move forward in a clear, wise way.

An Anti-Budget, on the other hand, is more of a big picture approach. You no longer have to track at the dollar for dollar level, as long as you’re not borrowing money or accessing savings to keep your monthly spending in line!

Matt proposes a 10-20-20-50 Approach: Giving (10%), Savings/Investing (20%), Fun (20%), and General Life Expenses (50%). (Are you in a debt-repayment phase? The 20% can be for debt repayment instead.)

Budgeting is not about the right app or system.

Don’t let the fear of the project keep you from starting. “It gets easier as you persevere,” Matt assures us. “First time, worst time. It’s true for grown-ups, too.”

What are the key first steps a homeschool family can take to bring order to their budget? {9:40}

Budgeting for the homeschool family:

- Pay yourself first (savings and investing)

- Automate everything you can (this frees up brain space to improve your budget)

- Switch from credit cards to cash/debit cards

- Make a plan before the month begins and track yourself against that plan

- Allow yourself a miscellaneous category, like a “mini-emergency fund” within your budget

This miscellaneous category can be from 5%-10% of your gross income, and can be used for unexpected expenses that come up (like dishwasher repairs). This resonates with my philosophy of the time budget for homeschool planning. Plan for the unexpected; give yourself margin.

I was blown away when Matt shared how his family saved $800 just from switching their mode of paying the same set of expenses from a credit card to cash! He said that “adding the extra friction to our spending was meaningful.” I’d say so!

Budgeting for Homeschool Families: investing in our children’s education without sacrificing our financial health {12:55}

“Assume you can do it fairly cheaply; like anything, it costs what you want it to cost. Start with cheap and then notice where the pain points are and add over time,” Matt advised.

Don’t let social media envy destroy your perspective on homeschooling. I notice often in my peers and in my own heart the worry that “if I don’t do what that family is doing my kid is missing out” or “I’m not a good homeschool mom if we don’t do that project/use that curriculum/take that class.” It’s just not true.

Matt also helpfully reminded us that there are many creative income opportunities along the way even within homeschooling. His wife, Charity, for example has been able to find a way to utilize CC for their children without additional cost to their family because of her own work there.

Budgeting for Homeschool Families: that dreadful Grocery Budget! {18:05}

Groceries for a homeschool family can be a killer to the budget, and that category can dramatically change over time!

I asked Matt for a realistic perspective on what groceries ought to cost. Sometimes it seems like estimates online either don’t take into account that my larger-than-average family is home all day every day, or they don’t take into account healthy eating. Matt’s reply? “$5-$7/person per day is a reasonable range” for a family’s grocery budget.

(We didn’t discuss this in the video, but my sister-in-law recommends Cheapskate Cook. She is a good resource for realistic, whole-food, budget-conscious food choices for a family.)

One simple way to save money on groceries? It’s not necessarily clipping coupons! Just figuring out which store to go to for which items can be helpful!

Walmart pickup has become a favorite grocery-budget hack for our family! I love that I can see our running total as I put the groceries in the online cart. It also keeps me from making as many spontaneous purchases.

What about saving for our kids’ future, whether college or something else? {23:30}

This may shock you: “Some level of retirement savings… and not having debt… are higher priorities than any kind of financial savings for your children,” Matt assures us.

Also, don’t get freaked out by the large price tags you often see for higher education. Listening to Matt’s perspective provided some much-needed right-sizing of my concerns for my children’s future.

How do we communicate a wise perspective about budgeting and finance to our children? How can we encourage them to work and manage their money wisely now and in the future? {28:50}

Teaching your children financial literacy is not a trick; you do it over time. Besides walking alongside and talking frankly with your children, seek out helpful mentors in your life who are willing to speak into your child’s life, consider things like “Project 23” in your co-op or homeschool group, or maybe look into Smart Money, Smart Kids.

What are some of Matt’s recommended books and resources in the budget/finance realm? {31:00}

For the total budgeting beginner, especially if you’re dealing with a lot of debt:

Total Money Makeover, Dave Ramsey

If you’re still a beginner, but you’re in control of your money:

The Automatic Millionaire, David Bach

Intermediate/Advanced options (please see video for Matt’s important caveats; additionally, please preview before sharing with your children):

The Simple Path to Wealth, Jim Collins

Your Money or Your Life, Vicki Collins

For teens:

The Richest Man in Babylon, George Clason

The Latte Factor, David Bach (narrative, fiction style)

Matt’s back with a mini-bonus episode! Here are 2 specific ways the Miner family develops and encourages financial independence in their children:

Bank of Dad: With the Bank of Dad, parents pay 10% interest on all money deposited there up to a maximum deposit of $1000. This teaches your children the power of compounding interest and lets their money earn money in a way you’re in control of. The Miner family encourages their children to take their second thousand dollars and invest in a credit union checking account, and then invest any additional future money in business or in some other long-term investment. This is a great teaching tool! And, bonus for parents: if your kids break off the car side mirror? Or crash their bike into the garage door? They have their own money to pay for it.

Private business and teaching the value of work: One of the Miner children has launched his own business as a small batch homeschool roaster. He orders green coffee with his own money and roasts it to order. The Miner’s daughter works as a regular after-school neighborhood childcare provider at 4-8 hr/week. The youngest Miner loves yard work, and works for his own family in their yard and in neighbor’s yards when the opportunity arises.

Another book recommendation: The $100 Start-Up by Chris Guillebeau contains ideas for micro-businesses, some of which are suitable for your children, and it might get their creative juices flowing!

Thanks, again, Matt for your willingness to come talk all things budgeting for homeschool families with us here at HumilityandDoxology.com!

Definitely reach out to Matt Miner with all your money-related questions {Web: Design Independence, LinkedIn, and the Work Pants Finance podcast)}. And please share this post with your friends!

Amy, it was a fun conversation. And your notes are amazing. No hyperbole: These are some of the best show notes I’ve read! You bring your writing excellence to the show notes! Thanks again for sharing time. I trust your readers and viewers will find value in the conversation.

Thanks, Matt, for the chat and the encouragement!

It’s vital that we teach our kids about money. Our American culture (and our own sinful nature) teaches us to spend everything we have. We need to develop self-discipline.